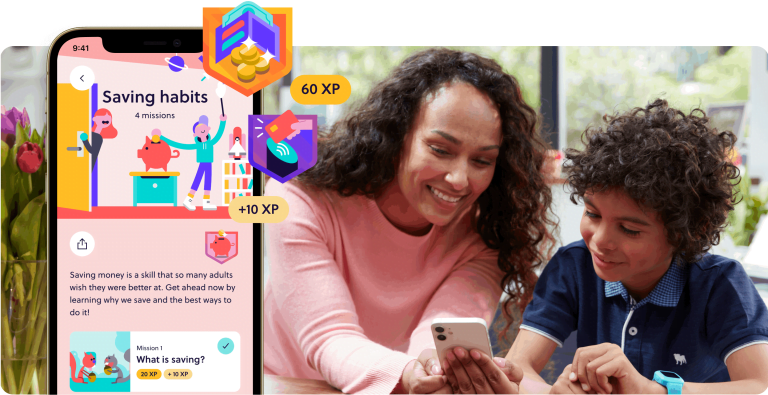

goHenry launched this tool to address the issue of financial literacy, which even some adults find difficult. According to a study conducted by the University of Cambridge, children form their...

Student debt is at an alarming high. Statistics have shown that in 2017 currently in the UK the average amount of debt for each of the graduates is £32,220. Some...

There are different options when it comes to getting a bank account for your kids. It’s tempting to go to the main stream high street banks but they tend to...

While college students need credit cards for various reasons, the most important reason is to built and reinforce a positive credit history. If handled in an improper manner, a credit...

Rooster Money, formally known as Rooster Bank, is a useful piggy bank website allowing children to learn the values of saving pocket money, gifts and allowances towards goals and targets....

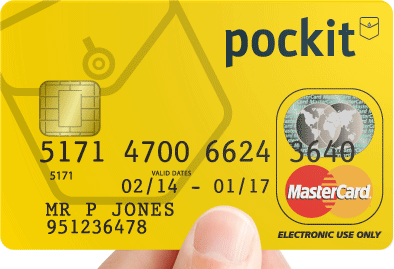

Pockit Credit Card? No Actually, Pockit Debit Card Although Pockit carries the MasterCard logo, it is tempting to think that the card is a credit card, when in fact it...

There is some debate as to whether a debit card for teens is appropriate. It seems like the concept divides opinion somewhat. In this blog post I take a look...

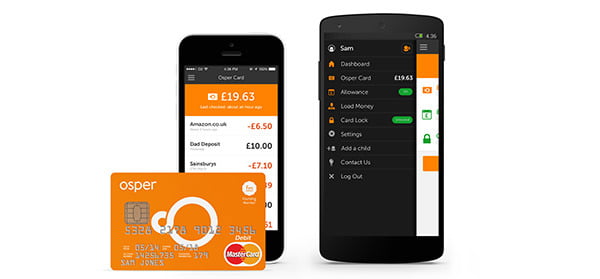

Are you looking to teach your children financial responsibility and the value of money? The Osper debit card and smartphone app can help! Most parents are looking for something that will...

There are many different methods you can use when it comes to teaching children about money. Offline or online, cash or electronic, financial education isn’t on the school curriculum. Maths...

Go Henry used to be called PKTMNY, (as in pocket money) when it was launched in November 2012. They have now rebranded as Go Henry which is a far catchier...

Go Henry isn’t the only option when it comes to helping to teach your child or children about managing their pocket money. We take a look at other Go Henry...

There are quite a few prepaid cards for teenagers, but there are so many different options out there. We take a look at the top selling cards so that you...

I have yet to find any other system out there like Go Henry. I think the creators have put a lot of thought into their product. There are financial products...

We mainly struggled because we operated without a budget or any controls in place with regard to spending. We definitely learned financial responsibility the hard way, and it was a...